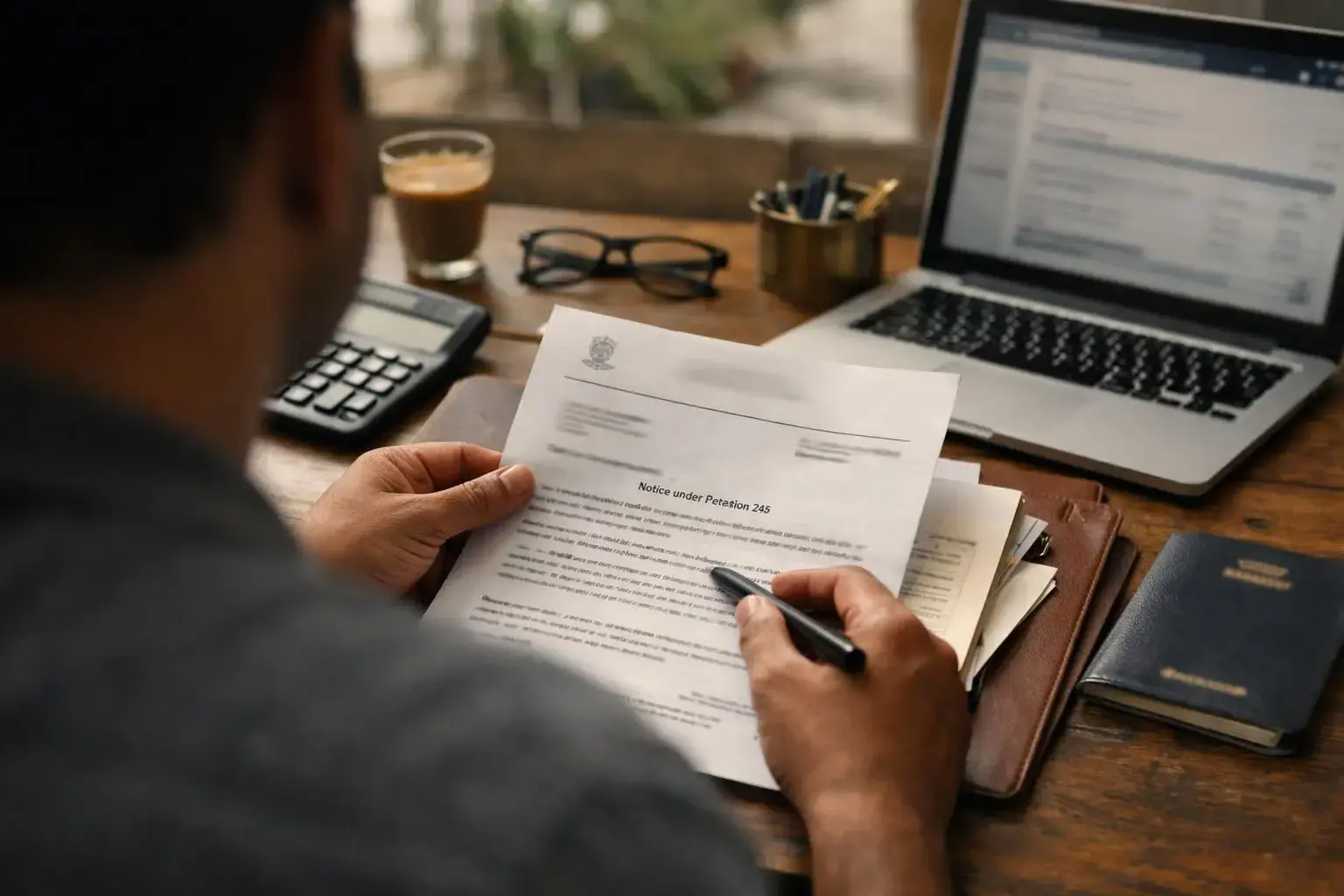

Understanding Notice under Section 245

Notice under Section 245 is a formal communication sent by the Income Tax Department to taxpayers in India. It informs the recipient that their income tax refund for the current financial year is being adjusted to cover unpaid tax demands from earlier years. This notice is issued under Section 245 of the Income Tax Act, 1961, which allows the department to set off refunds against outstanding tax liabilities.

Related glossary terms: Form 26AS, Notice under Section 143(1), Taxable Income.

The purpose of this notice is to ensure that taxpayers settle their dues before receiving refunds. For example, if a taxpayer has an unpaid tax demand from the previous assessment year, the department may use the refund amount from the current year to clear that demand. This process helps the government recover outstanding taxes efficiently without requiring additional legal action.

How Notice under Section 245 Works?

When the Income Tax Department identifies an unpaid tax demand in a taxpayer’s records, it first verifies the amount and checks if the taxpayer has a refund due for the current year. If both conditions are met, the department issues a Notice under Section 245. The notice specifies the amount of the outstanding demand, the assessment year it relates to. And the refund amount being adjusted.

Taxpayers receive this notice through their registered email address and can also view it in their e-filing account on the Income Tax Department’s portal. The notice provides a timeline for responding, usually 30 days, during which the taxpayer can either accept the adjustment or challenge it if they believe the demand is incorrect. If no response is received, the department proceeds with the adjustment.

For instance, if a taxpayer has a refund of ₹50,000 for the current year but owes ₹30,000 from a previous year, the department will adjust ₹30,000 from the refund and credit the remaining ₹20,000 to the taxpayer’s bank account. This adjustment is reflected in the taxpayer’s Form 26AS, which tracks tax credits and liabilities.

Why Notice under Section 245 Matters?

Notice under Section 245 is important because it ensures that taxpayers fulfill their tax obligations before receiving refunds. This helps the government maintain a steady flow of revenue and reduces the burden of chasing unpaid taxes. For taxpayers, the notice serves as a reminder to review their tax records and address any discrepancies or outstanding demands.

For local customers, Ignoring or missing this notice can lead to delays in receiving refunds. If the taxpayer believes the demand is incorrect, they must respond within the given timeframe to avoid automatic adjustment. This notice also provides an opportunity to correct errors, such as wrongly calculated demands or demands that have already been paid. Addressing these issues promptly can prevent further legal complications or penalties.

When Notice under Section 245 Matters Most?

Notice under Section 245 matters most when a taxpayer is expecting a refund but has unpaid tax demands from previous years. This situation commonly arises when taxpayers file returns but fail to pay the self-assessment tax or when discrepancies in tax calculations lead to demands raised by the department. It's also relevant for taxpayers who have not responded to earlier notices or have unresolved disputes with the department.

Taxpayers should pay special attention to this notice if they have changed jobs, have multiple income sources. Or have filed revised returns in the past. These scenarios often lead to discrepancies in tax records, which can result in demands being raised. And senior citizens, freelancers. And business owners who may have varying income levels should review the notice carefully to ensure the demand is accurate and justified.

If the taxpayer disagrees with the demand, they should gather supporting documents, such as bank statements, challans. Or previous year’s tax returns, to substantiate their claim. Responding to the notice with accurate information can help resolve the issue without further legal action or delays in refund processing.